Ranked #41 of 51 by Cost

2026 Massachusetts Car Insurance Calculator

Estimate your monthly premium based on The Bay State averages

Rate Calculator

Local insurance tip

Massachusetts is a no-fault state with mandatory Personal Injury Protection, but it also operates a state-regulated insurance market where rates are closely overseen by the Division of Insurance. Shopping between carriers at renewal is especially valuable in Massachusetts. Rate differences between insurers for identical drivers can be substantial and the competitive market rewards drivers who compare quotes rather than auto-renewing.

Cost Breakdown

| Coverage | Monthly | Description |

|---|---|---|

| MA minimum | $80 | Legal bare minimum (liability only) |

| Standard liability | $128 | High Liability, no physical damage |

| Full coverage | $170 | Comprehensive ($500 ded.) |

| Premium protection | $231 | Max liability ($250 ded.) |

| Age | Risk | Monthly |

|---|---|---|

| 16-19 | Very high | $502 |

| 20-24 | High | $281 |

| 25-54 | Standard | $170 |

| 55-69 | Low | $162 |

| 70+ | Moderate | $213 |

| Violation | Risk | Monthly |

|---|---|---|

| Clean | Standard | $170 |

| Speeding Ticket | Moderate | $207 |

| At-Fault Accident | High | $252 |

| DUI / DWI | Very high | $485 |

Massachusetts Snapshot · July 2026

$170/mo

State avg (-31% US AVG)

#41

National Rank

110%

County Spread

Rate by Neighboring States (6)

State Insight

Massachusetts is cheaper than most might expect given Boston's reputation. New York is dramatically more expensive. Connecticut and Rhode Island both sit meaningfully above Massachusetts. New Hampshire and Vermont are the most affordable neighbors, a reflection of their rural character and lower litigation activity.

Rate by Cities (Top 50)

Compared to MA avg ($170)

City Insight

Dorchester and Brockton lead the state by a significant margin, their concentrated urban density and high uninsured driver exposure pushing rates well above even Boston proper. The contrast with western Massachusetts cities like Andover, Westfield and Franklin is striking — those markets feel closer to New Hampshire than to the eastern corridor.

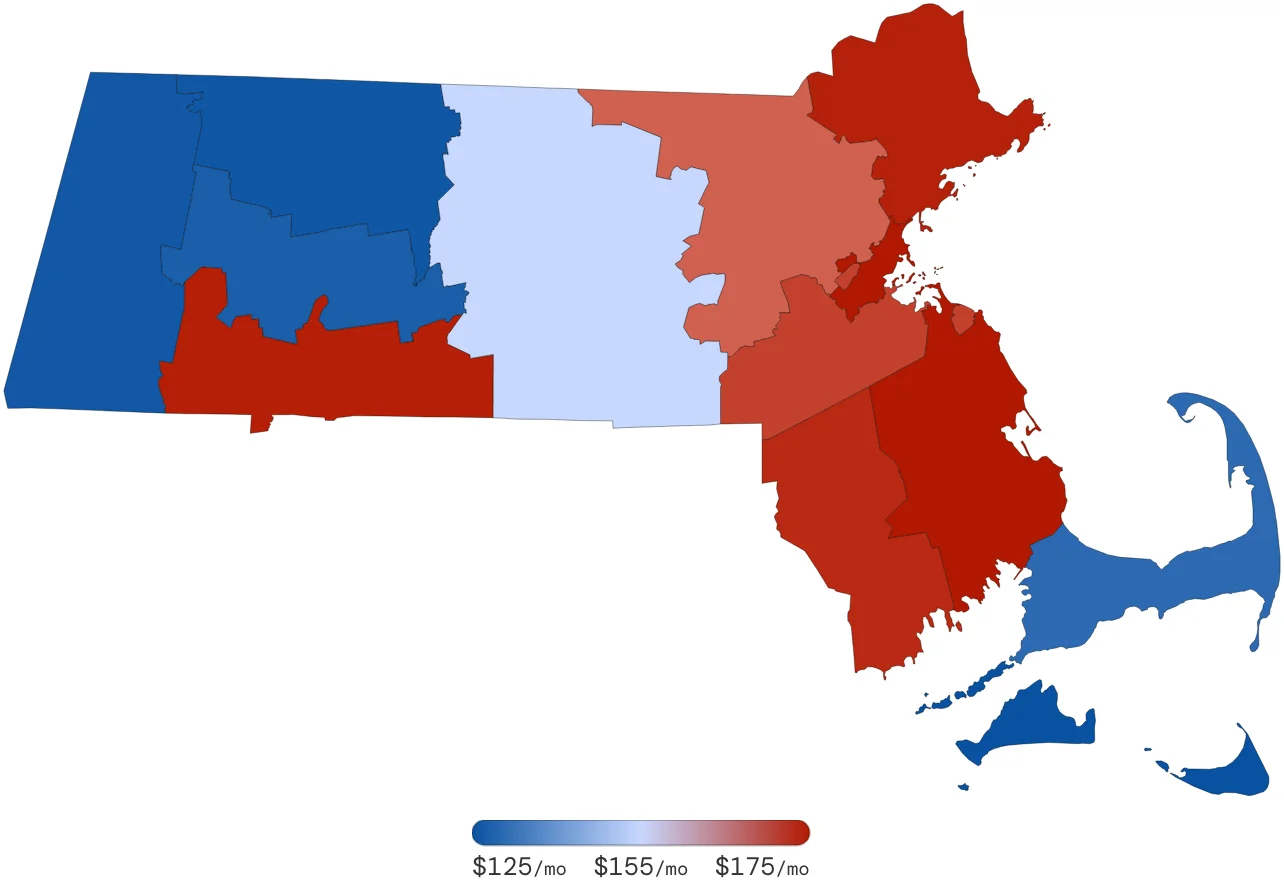

Rate by Counties (14)

Compared to MA avg ($170)

County Insight

Suffolk County drives the state's high-rate tier, anchored by Boston and its inner neighborhoods. Nantucket and Dukes counties are the most affordable in the state, an unusual dynamic where island geography limits traffic density and claim frequency far below the mainland average. Berkshire and Franklin counties in western Massachusetts sit well below the state average, reinforcing the sharp east-west divide.

What Every Massachusetts Driver Needs To Know

What are the minimum car insurance requirements in MA for 2026?

Massachusetts requires 20/40/5 liability minimums, plus $8,000 in Personal Injury Protection (PIP) and $20,000/$40,000 in Uninsured Motorist coverage. Massachusetts is a no-fault state, meaning PIP pays your medical bills regardless of fault up to the policy limit.

Is Massachusetts a no-fault state?

Yes, Massachusetts is a no-fault state, meaning your own PIP pays the first $8,000 of your medical bills and a portion of lost wages after an accident, regardless of who caused it. You can step outside the no-fault system and sue the at-fault driver for pain and suffering only if your medical expenses exceed $2,000 or your injury involves a fracture, permanent disfigurement, or loss of a body part.

Why is Boston car insurance so expensive compared to the rest of Massachusetts?

Boston's insurance costs reflect a combination of factors unique to the city: extreme traffic density, particularly in the tunnel and bridge corridors of the Big Dig infrastructure, high auto repair labor rates, active personal injury litigation in Suffolk County courts and vehicle theft rates that significantly exceed the state average. Drivers who garage their vehicle outside the city limits, even in nearby suburbs, often pay meaningfully less for the same coverage.

What are the penalties for driving uninsured in Massachusetts?

Massachusetts takes uninsured driving very seriously. A first offense results in a fine of $500–$5,000, up to one year in jail and license suspension for 60 days. Reinstatement requires proof of insurance and payment of fees. Massachusetts uses an electronic verification system and insurers report policy cancellations to the RMV promptly, meaning lapses are detected quickly even without a traffic stop.

Sources: Massachusetts RMV